IPO Pops, Dutch Auctions & How to Steal an Election

IPO Pops, Dutch Auctions & How to Steal an Election

There’s been a lot of talk about direct listings and SPAC’s recently but IPOs are still the main way companies go public. This week’s focus starts with problems within the public funding space and what companies like Google have done to try and solve them. Seeing as how November is coming up soon, the third question today deals with various election fraud strategies seen around the world

IPO Pops (1 min)

Dutch Auctions (2 min)

How to Steal an Election (2 min)

Why is there usually an "IPO pop" when a company goes public?

When a company decides to go public it starts by hiring banks to act as underwriters. The chosen underwriting banks will try to determine a fair price for the company and then pitch and sell shares to institutional investors who commit to buying large chunks of the impending share issuance. On average institutional investors get a price per share 13-15% below what the opening price of the stock ends up being (and often the discrepancy is much higher). This is known as the "IPO pop".

The company wants to maximize its windfall from selling shares and wants to make sure that their underwriters are not pricing their shares too low (which would be demonstrated by a higher IPO pop on opening day). Meanwhile, the institutional investors who the underwriters are pitching to before the IPO want the lowest price possible so that they can see their shares rise in value once they're publicly available.

The underwriters are ostensibly clients of the company they are representing but in practice there's an incentive misalignment between the two. The underwriters are only ever going to take this specific company public once. However, they are constantly pitching new companies to the same groups of institutional investors. In essence they are playing a repeat game with these institutional investors where it's beneficial for both sides for there to be an "IPO pop" since the investors make money and the underwriters have an easy outlet to sell shares to for future companies they represent.

Thanks to Matt Levine's ever-insightful writing for being the source of the dynamic between underwriters and companies.

In Other Words

Underwriters hired by a company that wants to IPO have a strong incentive to underprice company shares to ensure that their "real" customers, the institutional investors they sell too, lock in a profit when the newly issued shares debut. This is because underwriters only ever IPO a company once while they are continuously pitching shares to the same groups of institutional investors and therefore need to foster good relationships with them to ensure a continued source of demand for future IPO issuances.

What can be done to reduce the amount of capital that companies forgo due to the "IPO pop"?

Many market observers have lamented the fact that IPOs leave so much money on the table for the companies going public. The average IPO pop (price above IPO that newly public companies trade at) is 13-15% but it is often higher for certain industries like tech. A large IPO pop means, "[that] the company could have sold its shares for a higher price and raised more money". To take a recent example, Lemonade IPO'd at $29 (raising $319 million) and its share price opened at $50 before closing at $69 on its debut day. Clearly there was demand for their shares at a price far in excess of what their bankers were able to secure. Had Lemonade been able to price according to the true demand demonstrated on opening day they could have raised anywhere between $550-750 million. Instead that change in value accrued to its shareholders (including the institutional investors who bought in during the IPO process at $29).

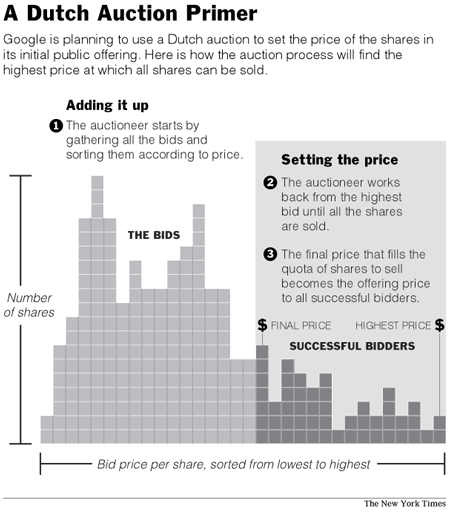

But IPOs don't have to be run in the traditional way. In fact, Google's IPO in 2004 is a great example of how a company can IPO and still capture a lot of the value for themselves (at least in theory). Instead of going through the traditional IPO process, Google borrowed a method of price discovery they used in their ad business called a dutch auction.

Google allowed anyone to bid on the number of shares they would be committing to buy as well as the price that they would be willing to pay. After everyone had submitted their bids Google set the price of their shares at the highest price that would still result in all shares in the offering being sold (known as the market-clearing price).

Let's say you want to sell 50 shares in an IPO and you have 3 bidders. Alice bids $100 a share for 25 shares, Bob bids $80 for the same number, and Charlie bids $120 again for the same number. In the dutch auction process, Alice and Charlie would be allocated 25 shares each at $100. Both Alice and Charlie pay $100 because this is the market-clearing price (the lowest price at which all 50 shares are sold).

In Google's case, they were targeting a price range of $108 to $135 but the week before the IPO many of the institutional investors who had agreed to "bid" on shares at these price levels instead mysteriously opted to resubmit their bids at $85. (see here for speculation on why) This meant that Google opened at $85 and promptly experienced an IPO pop sending it above $100 on opening day (meaning they failed to capture all of the upside that was technically available to them since they failed to properly price their IPO). Although Google might not have been able to shift the way IPOs were conducted, they at least proved that the dutch auction system was a viable alternative to traditional opaque IPO pricing.

In Other Words

Recently companies have been exploring alternatives to the IPO process because they typically leave money on the table through underpricing of their shares and high banker fees. Google attempted to solve this problem in 2004 using a process borrowed from its advertising unit called the Dutch Auction. However, it too ended up leaving money on the table because its stock promptly shot up 18% on opening day, indicating that it was not able to successfully achieve true price discovery.

What are the methods countries and candidates use to sway elections across the world?

Seymour Hersh, a former reporter for the Washington Post, talks about his experience with elections in the Middle East in his autobiography Reporter: "[Nasrallah, the leader of Hezbollah in Lebanon] also assured me that the Iraqi opposition would win control of the Iraqi parliament in the 2005 election there... Predicting an election victory was one thing, but Nasrallah's prediction came within one-tenth of a point of the winning margin. I concluded there was much we Americans did not know about fixing elections". The fact that a leader of a neighboring country was able to demonstrate foreknowledge of the election outcome to such a degree speaks volumes about the value of the elections being held in Iraq at the time.

The EIU Democracy Index defines hybrid democracies as those "with regular electoral frauds, preventing them from being fair and free democrac[ies]" and as of 2019, it counts 37 different countries in this category. However, not all election fraud is created equally. There exists a wide middle ground between brazenly fixing an election (see above or Egypt) and trying to subtly (and sometimes not so subtly) influence public opinion through the use of social media or more terrestrial means.

In 2016 Bloomberg interviewed a former political operative named Andrés Sepúlvada who divulged, "My job was to do actions of dirty war and psychological operations, black propaganda, rumors—the whole dark side of politics that nobody knows exists but everyone can see. When the candidates’ teams prepared policy speeches, Sepúlveda had the details as soon as a speechwriter’s fingers hit the keyboard. Sepúlveda saw the opponents’ upcoming meetings and campaign schedules before their own teams did."

Hacking into candidates and their strategist’s phones and emails wasn't even about getting ahead, sometimes it was just evening the playing field. As another former political consultant in the article says, "It goes with the trade in Latin America: Having a phone hacked by the opposition is not a novelty. When I work on a campaign, the assumption is that everything I talk about on the phone will be heard by the opponents."

Beyond hacking for information or donor lists the other major goal Sepúlvada outlined was finding creative ways to suppress turnout for the opposition. "On election night, he had computers call tens of thousands of voters with prerecorded phone messages at 3 a.m. in the critical swing state of Jalisco. The calls appeared to come from the campaign of popular left-wing gubernatorial candidate Enrique Alfaro Ramírez. That angered voters—that was the point—and Alfaro lost by a slim margin."

Of course, these techniques aren't unique to the political atmosphere in Latin America. Often associated with African elections, turning off the internet helps mask accusations of electoral fraud, prevent dissidents from gathering together, and helps keep the opposition in check. In 2019 alone, "Algeria, Burundi, Democratic Republic of Congo, Eritrea, Ethiopia, Gabon, the Gambia, Uganda, and Zimbabwe have all shut down domestic access to the internet during elections".

It would appear that Hersh was right when he said that there is much we have to learn about fixing elections in America.

In Other Words

Influencing and hacking an election spans a wide variety of outcomes such as disinformation and social media influence campaigns, hacking of candidates phones/emails and donor lists, sophisticated voter suppression techniques, turning off the internet to prevent the spread of information and communication, to finally just fixing the election results and calling it a day. It would appear that many countries are democracies in name alone.

That’s all for this week. Thanks for making it this far and I hope you found these answers as interesting to read as I found them interesting to write.

As always,

Roosh → You

I guess if you know your political rivals are listening in to everything you say on the phone, you could begin to confuse them with lies about what your campaign is planning! Probably a confusing system to your own team though...